The Property Planner’s Monthly Market Update: February 2026

- Property Planning Australia

- Mar 17

- 3 min read

Updated: Mar 27

Welcome to the Property Planner’s Monthly Market Update, your comprehensive resource for the latest insights and trends in the real estate and economic landscape!

Stay informed and ahead of the curve with our expert analysis, helping you make well-informed decisions in the ever-evolving property market.

Perth Just Won’t Quit

Perth again led the capitals in February, posting 2.3% growth for the month, working out to be 24%+ when annualised.

Even after this sustained run, the market continues to be supported by very low supply, with Perth listing levels 48% below their five-year average.

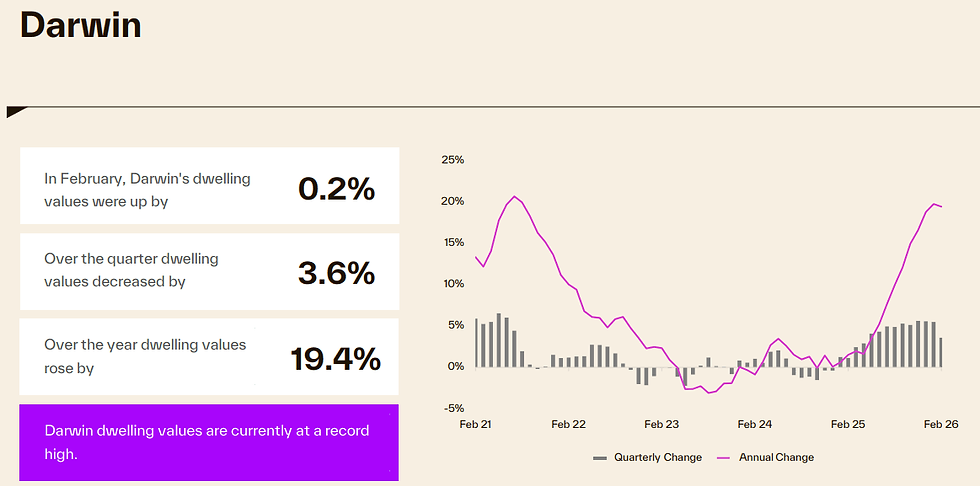

Darwin May Be Hitting a Ceiling

Darwin rose just 0.2% in February, a noticeable slowdown from the 1%+ monthly pace it had been posting.

Even so, annual growth is still sitting at around 19.4%, so the question is less about whether Darwin has performed well and more about whether momentum is now starting to fade.

Is Hobart Starting to Turn?

Hobart posted 1.2% growth in February, which equates to roughly 14% when annualised.

Vacancy rates are sitting at just 0.4%, one of the lowest rates in the country and that tightening rental backdrop is one of the clearest signs the market may be starting to shift direction.

Regional Markets Are Still Outperforming

Combined regional markets are up 11.1% over the past 12 months, compared with 9.6% across the capitals, showing that regional Australia is still outperforming overall.

Regional Victoria was the weakest regional performer in February at 0.6%, while regional Western Australia and regional South Australia led over the past three months.

Rental Vacancies Remain Critically Tight

Rental supply remains extremely constrained.

Vacancies tightened further across almost every market, with national vacancy rates sitting around 1.2%.

This helps explain why rental pressure remains elevated and why housing continues to be such a strong inflation driver.

More Rate Rises Are Being Priced In

Following the RBA’s 17 March increase, the cash rate now sits at 4.10%.

Markets are still pricing in a high probability of two further rate rises, with one hike expected by August and a second potentially by year-end.

This continues to create a more difficult environment for borrowers, puts further pressure on borrowing capacity and may cause some buyers to delay decisions while others move quickly before conditions tighten again.

Buyer Sentiment Is Weakening

The time-to-buy-a-dwelling index fell from 84 to 82.9 in March, remaining well below its long-run average of 120.

Among mortgage holders, sentiment dropped 16% to 73.

The weakest buyer sentiment was found in states with continued strong price growth: in Queensland 76 and in Western Australia to 65.

AI and Job Losses Are a Risk Worth Watching

AI-related job disruption is becoming harder to ignore.

Recent examples include Block cutting 40% of its workforce, WiseTech cutting 2,000 jobs globally or 29% of staff, and CBA cutting 300 jobs while investing heavily in AI systems and workforce transformation.

It is still early days, but this is a theme worth watching closely.

Want to learn more? Listen to the Property Trio Podcast

Reach Out to Us

If you would like to discuss your next steps, property plans, and mortgage strategy, get in touch with us today. Our team of experts is here to guide you through the complexities of the market and help you achieve your property goals.